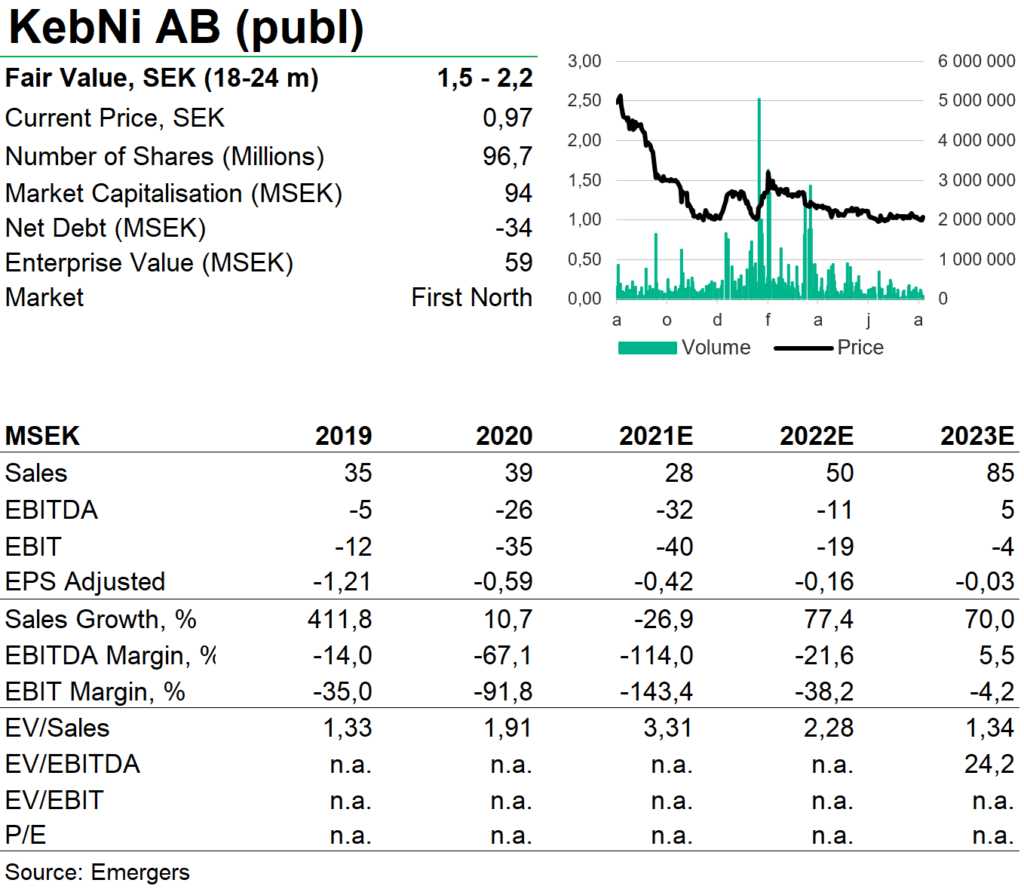

Strong momentum in build-up behind the lull this quarter

The report for the second quarter reflects a high level of internal activity at KebNi, demonstrating excellent potential to re-style the company into a more sales-oriented organization with a broader and more current product offering, including everything from the new 1.8 meter drive-away antenna, an IMU offering that highlights the forefront of technology with the launch of NG IMU, and a sales organization with a tripled reach in terms of partner presence by 2022. At the same time, short-term growth continued to weaken in the second quarter, with basically non-existent sales, earnings of SEK -10 million and operating cash flow of SEK -17 million.

Mixed performance in the existing portfolio

In addition to the final delivery to IAI during Q2 2021 and scheduled deliveries of IMU prototypes to SAAB, Satmission is now preparing a road show during the autumn that should be able to make an impact on sales in the medium term. At the same time, development work is underway on the company’s own IMU application for monitoring scaffolding, which is expected to be launched in 2022. Although we expect small volumes initially, our calculations show (see our most recent update Scaffolding focus in new vertical with great potential) annual revenue potential of SEK 100 million, and the application will be able to expand to real-time monitoring of a variety of other areas with little or no modification.